Transaction volume is still way down.

Vacancy is up.

Costs to stabilize remain challenging.

Existential risk? Still ever-present.

And pricing? That depends on who you ask.

Toby Jorgensen recently published a compelling article on CoStar Insight: “Several Distressed Deals Highlight the Long Road Ahead for Office Sales.” It’s a sobering reminder of the road we’re on in the Nashville office market.

If you're a buyer, this is a season for discipline. Strategy often means waiting for sellers—and their price expectations—to catch up to market reality.

If you're a seller, this is a season for recalibration. Understand how a lender and an appraiser will underwrite your property. Because that’s exactly how a buyer will evaluate it too.

As borrowing costs rise and vacancy rates climb to multi-decade highs, investor appetite—at pre-2023 prices—has understandably thinned.

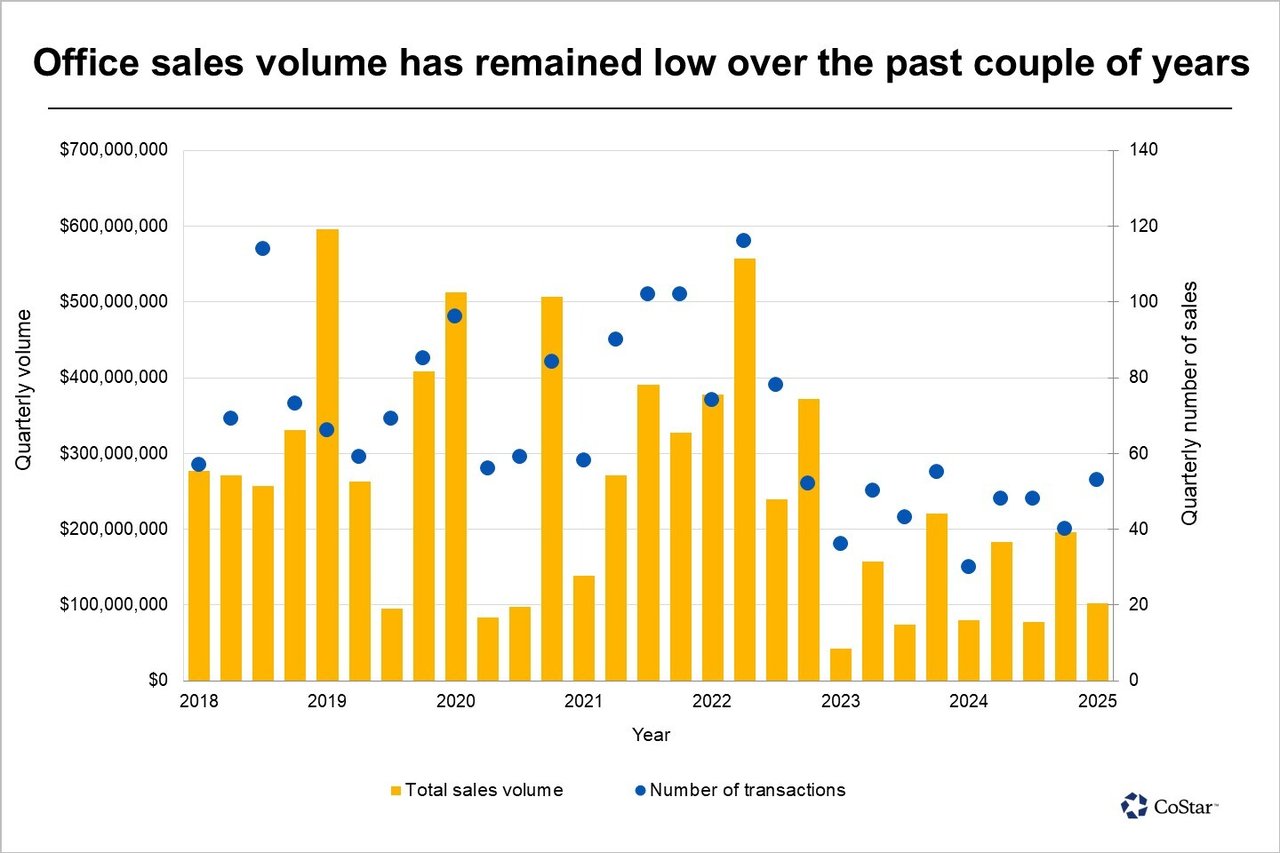

According to CoStar:

“During 2021 and 2022, quarterly transaction volume averaged $334 million across 84 deals. Since 2023, that number has dropped to $126 million and just 45 deals per quarter.”

That’s a 62% decline in transaction volume and nearly half the activity.

Why?

-

Rising interest rates

-

Stubborn seller pricing

-

Leasing demand concentrated in smaller, local users

-

Post-COVID shifts in office utilization

-

Lenders pulling back

-

Buyers seeking risk-adjusted returns

The New Reality: Real Deals, Real Discounts

Recent trades in Nashville show the dramatic correction in values:

-

Philips Plaza (445,000 SF) sold for $17M — an 85% drop from its previous valuation. It was 49% leased.

-

Parkway Tower (205,000 SF, vintage 1968) sold for $12.5M — a $21M loss since 2019.

-

Citizens Plaza (270,000 SF) fetched $16M — less than the state paid in 1986. It was nearly vacant.

-

111 Westpark (100,000 SF) sold for $6.3M — just $63/SF.

These aren’t just “distressed” deals—they are signals. Vacant space, functional obsolescence, and market skepticism about the future of office are real value drivers now.

Buyers are disciplined.

Lenders are sober.

Sellers are (learning to be) patient.

Buyers today understand what it takes to stabilize a mid-rise office:

-

Build out spec suites

-

Create multi-tenant corridors

-

Front the tenant improvements & leasing commissions

-

Wait 18–36 months to stabilize occupancy

-

Market heavily, often with incentive commissions

That level of effort requires a meaningful discount on entry price. Yield must be built in from day one—not hoped for in year three.

So What’s Next?

Some outliers remain: parcels in SoBro, the East Bank, or near Oracle’s campus—where redevelopment or zoning upside provides a different calculus.

But for the majority of buildings, reality is being measured by:

-

Current rent rolls

-

Actual leasing income

-

Reasonable absorption timelines

-

Renovation costs

-

Cap rate expectations in a tighter lending environment

If you own, occupy, or invest in Nashville office space, this is a moment for clarity, strategy, and honest positioning.

Let’s talk about where the market’s headed—and how you can be ready.